从世界黄金协会(WGC)黄金在虎年新的报告预测中,在中国的黄金消费中,作为首饰的需求不断增加,实物性资产投资和工业用途的结果,可能在未来10年其黄金消费量增加两倍,

这一预测似乎是合理的,因为中国经济深刻的演变,即国内消费正在取代出口的调整,因为愈来愈穷的中国人转移成中产阶层,并由此进入富人的行列,成为新的财富增长的引擎。

在中国每年数以千万计的人正在加入中产阶级行列,有人估计,他们人口的数目已经超过整个美国人口,而且在未来的10年时间里,可能还会增加一倍。

由此导致的结果是这些人将购买更多更好与自身身份配备的宽敞家园。他们已经使得中国成为世界上最大的汽车消费市场和一个西方人看到的奢侈品品牌的大国,在极可能广泛的省会城市中你亦可以看到这些熟悉的品牌名字。

我们发现中国有一个多世纪之久的黄金文化的亲和力,所以可以预见的是未来将会有更多的中产阶层和富人储备更多的黄金。

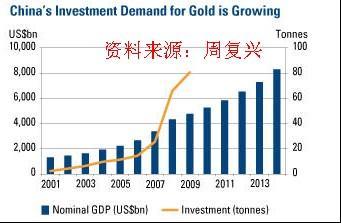

上述图表显示,投资黄金的需求是如何激增的:在2001年需求量只是很小的份额,而在去年它已经上升到80吨(260万金衡盎司),尤其是在2007年黄金市场开放并被理性投资者认可之后,可以发现其回升幅度越来越大,而同期中国国内生产总值大约增长了三倍。中华民族在世界上是有名的高储蓄率国家,图表显示了黄金如何作为市场投资者,成为其必要的投资组合的一部分和重要的不断增长的财富储蓄商店。

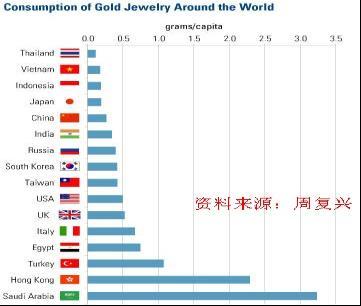

比较接下来的图表,中国的年黄金首饰消费量,已经超过12个以上的其他国家。去年中国消耗了347吨的珠宝,其中有30吨的数目是高于这个国家黄金年生产量(列世界第一)。但在人均占有的水平上,中国却靠近此列表的底部。

世界黄金协会指出,如果中国匹配沙特阿拉伯人均比例的话,在人均基础上的水平,将额外消耗每年4000吨的黄金首饰,这比去年的整个世界(3386吨)还要高,因此,即使是最热情的黄金信徒,更可能同意这不是一个现实的数字。

但由于预测说,中国的中产阶级将在未来10年,主导中国的经济增长,由此带来更大的财富分配,这不是牵强附会的,同时亦认为它的黄金消费量也可能增加一倍。

但是,国的国内黄金产量可能跟得上其需求增长,这却是牵强的,越来越多的世界黄金产量(我们看到它是呈多年下降趋势的)都必须转移至中国市场,在未来数年,其结果可能对黄金价格产生重大影响,然而你又将作何感想呢?

为便于读者更好理解,附上原译文如下:

China Is Gold’s Future

The new report “Gold in the Year of the Tiger” from the World Gold Council (WGC) predicts that gold consumption in China could double in the coming decade as a result of rising demand for jewelry, hard-asset investments and industrial uses.

This forecast seems reasonable, and it lines up with what I’ve long been saying about the profound evolution in China’s economy – domestic consumption is replacing exports as the growth engine as more poor Chinese move up into the middle class and from there into the ranks of the wealthy.

Tens of millions of people in China are joining the middle class every year – by some estimates, they already number more than the entire U.S. population and could double in the next decade.

They are buying more spacious and better-outfitted homes. They have made China the world’s largest automobile market, and a wide range of brand-name Western luxury items are available even in provincial cities.

China has a centuries-long cultural affinity for gold, so it makes sense that more middle class and wealthy would mean more gold sales.

The line on the WGC chart above shows how investment demand for gold has rocketed up from next to nothing in 2001 to 80 tonnes (2.6 million troy ounces) last year, with the sharpest upswing coming after trading rules were liberalized in mid-2007. Over the same period, China’s GDP roughly tripled. The Chinese are famous for their high savings rate, and the chart shows how important gold has become as a store of their growing wealth.

The next chart compares China’s annual gold jewelry consumption to more than a dozen other countries. Last year, China consumed 347 tonnes in jewelry, which was about 30 tonnes more than the country’s total gold production (tops in the world). But on a per-capita basis, China is near the bottom of this list.

The World Gold Council points out that, if China matched Saudi Arabia on a per-capita basis, it would consume an additional 4,000 tonnes of gold jewelry each year. That’s more than last year’s demand for the entire world (3,386 tonnes), so even the most enthusiastic gold devotees would probably agree that it’s not a realistic number.

But given projections that the Chinese middle class will double in the next decade as China’s economic growth generates a wider distribution of wealth, it’s not farfetched to think that its gold consumption could also double.

It is farfetched, however, to think that China’s domestic gold output could keep pace with demand growth – more and more of the world’s gold production (on a declining trend for years) would have to be diverted to the Chinese market, and the result could be a significant impact on gold prices in the years to come.

http://blog.sina.com.cn/s/blog_64453f140100ibyx.html