本文译自英国卫报,作者为美国总统奥巴马经济顾问委员会主席,也是专门研究“大萧条”的学者之一的克里斯蒂娜.罗默女士。

韩和元的观点:http://guancha.gmw.cn/content/2008-12/19/content_870904.htm

凯恩斯救活过1930年代大危机是天大的误会

《经济与财富通讯》:但凯恩斯的方法观的确救活过1930年代的那场大危机?

韩和元:那是一场莫大的误会,或者说其本身就是一场弥天大谎,读读罗斯福总统的传记我们就知道,那场危机的最严重的时期是在1937-1938年之间,而这个时点,凯恩斯的那本《通论》已经出版了,他的观点已经被罗斯福所采纳了,那点看的出来呢?对预算的态度,在1935年凯恩斯没有向总统先生推销他的主张以前,总统采取的是均衡预算,而到1936年后采取的却是大幅度的赤字预算,而赤字预算正是凯恩斯的认为干预的精髓。但真相却是,大量的政府投资,加剧了原本已经恶化的供需结构,使得产能严重过剩,为此罗斯福总统不得不承认,1938年的美国“消费者购买力薄弱令美国经济因消费者需求不足陷入困境!”但罗斯福很幸运,凯恩斯也很幸运,随着战争的扩大,各交战国的物资需求,终于让美国的那些过剩产能得到了应用,深陷战争的英国、法国、中国和日本(日本之所以要与美国交战,原因就在于美国拒绝再为他提供物资,日本认为美国的这一行动伤害到他的利益)的购买力取代了美国国内那薄弱的消费力而令美国经济因消费者需求增强而走出困境!

而到了1990年代,日本也爆发了经济危机,日本严格的遵照揩恩斯路线,采取大量大幅度的赤字预算,扩大公共支出,通过零利率等手段来干预需求面,但成绩却乏善可陈,日本为此失落了10年。

《经济与财富通讯》:从这些历史经验来看,凯恩斯救不了谁?

韩和元:对。其实,现在大家之所以都来膜拜凯恩斯,原因是基于人们对新自由主义的失望,就象中国台湾,并不是因为人们对国民党有什么好感,而只是因为人们对民进党彻底的失望,当人们所能够做的是二选一时,那么只好选一个自认为不那么坏的了。这就是民主的弊端之一,两个都是烂苹果,但你还是必须得选一个,这就是你民主权利的全部。

英文原文:

Economics focus

The lessons of 1937

Jun 18th 2009

From The Economist print edition

In a guest article, Christina Romer says policymakers must learn from the errors that prolonged the Depression

Christina Romer is the chairwoman of Barack Obama's Council of Economic Advisers and a scholar of the Depression

Christina Romer is the chairwoman of Barack Obama's Council of Economic Advisers and a scholar of the DepressionAT A recent congressional hearing I cautiously noted some “glimmers of hope” that the economy could stabilise and perhaps start to rebound later in the year. I was asked if this meant that we should cancel much of the remaining spending in the $787 billion American Recovery and Reinvestment Act. I responded that the expected recovery was both months away and predicated on Recovery Act spending ramping up greatly. Only later did it hit me that I should have told the story of 1937.

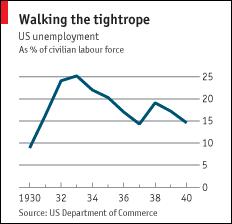

The recovery from the Depression is often described as slow because America did not return to full employment until after the outbreak of the second world war. But the truth is the recovery in the four years after Franklin Roosevelt took office in 1933 was incredibly rapid. Annual real GDP growth averaged over 9%. Unemployment fell from 25% to 14%. The second world war aside, the United States has never experienced such sustained, rapid growth.

However, that growth was halted by a second severe downturn in 1937-38, when unemployment surged again to 19% (see chart). The fundamental cause of this second recession was an unfortunate, and largely inadvertent, switch to contractionary fiscal and monetary policy. One source of the growth in 1936 was that Congress had overridden Mr Roosevelt’s veto and passed a large bonus for veterans of the first world war. In 1937, this fiscal stimulus disappeared. In addition, social-security taxes were collected for the first time. These factors reduced the deficit by roughly 2.5% of GDP, exerting significant contractionary pressure.

Also important was an accidental switch to contractionary monetary policy. In 1936 the Federal Reserve began to worry about its “exit strategy”. After several years of relatively loose monetary policy, American banks were holding large quantities of reserves in excess of their legislated requirements. Monetary policymakers feared these excess reserves would make it difficult to tighten if inflation developed or if “speculative excess” began again on Wall Street. In July 1936 the Fed’s board of governors stated that existing excess reserves could “create an injurious credit expansion” and that it had “decided to lock up” those excess reserves “as a measure of prevention”. The Fed then doubled reserve requirements in a series of steps. Unfortunately it turned out that banks, still nervous after the financial panics of the early 1930s, wanted to hold excess reserves as a cushion. When that excess was legislated away, they scrambled to replace it by reducing lending. According to a classic study of the Depression by Milton Friedman and Anna Schwartz, the resulting monetary contraction was a central cause of the 1937-38 recession.

The 1937 episode provides a cautionary tale. The urge to declare victory and get back to normal policy after an economic crisis is strong. That urge needs to be resisted until the economy is again approaching full employment. Financial crises, in particular, tend to leave scars that make financial institutions, households and firms behave differently. If the government withdraws support too early, a return to economic decline or even panic could follow. In this regard, not only should we not prematurely stop Recovery Act spending, we need to plan carefully for its expiration. According to the Congressional Budget Office, the Recovery Act will provide nearly $400 billion of stimulus in the 2010 fiscal year, but just over $130 billion in 2011. This implies a fiscal contraction of about 2% of GDP. If all goes well, private demand will have increased enough by then to fill the gap. If that is not the case, broad policy support may need to be sustained somewhat longer.

Perhaps a more fundamental lesson is that policymakers should find constructive ways to respond to the natural pressure to cut back on stimulus. For example, the Federal Reserve’s balance-sheet has more than doubled during the crisis, drawing considerable attention. Monetary policymakers have made it clear that they believe continued monetary ease is appropriate. Moreover, the Fed’s credit programmes are to some degree self-eliminating: as demand for its special credit facilities shrinks, so will its balance-sheet. But now may also be a sensible time to grant the Fed additional tools to help its balance-sheet contract once the economy has recovered. Some have suggested that the Fed be authorised to issue debt, as many other central banks do. This would enhance its ability to withdraw excess cash from the financial system. Granting such additional tools now could provide confidence that the Fed will be able to respond to inflationary pressures, without it having to create that confidence by actually tightening prematurely.

Fiscal health check

Now is also the time to think about our long-run fiscal situation. Despite the large budget deficit President Obama inherited, dealing with the current crisis required increasing the deficit substantially. To switch to austerity in the immediate future would surely set back recovery and risk a 1937-like recession-within-a-recession. But many are legitimately concerned about the longer-term budget situation. That is why the president has laid out a plan to shrink the deficit he inherited by half and has repeatedly emphasised the need to reduce the long-term deficit and put the debt-to-GDP ratio on a declining trajectory. In this regard, health-care reform presents a golden opportunity. The fundamental source of long-run deficits is rising health-care expenditures. By coupling the expansion of coverage with reforms that significantly slow the growth of health-care costs, we can dramatically improve the long-run fiscal situation without tightening prematurely.

As someone who has written somewhat critically of the short-sightedness of policymakers in the late 1930s, I feel new humility. I can see that the pressures they were under were probably enormous. Policymakers today need to learn from their experiences and respond to the same pressures constructively, without derailing the recovery before it has even begun.